Loading...

10 August 2026 / Report

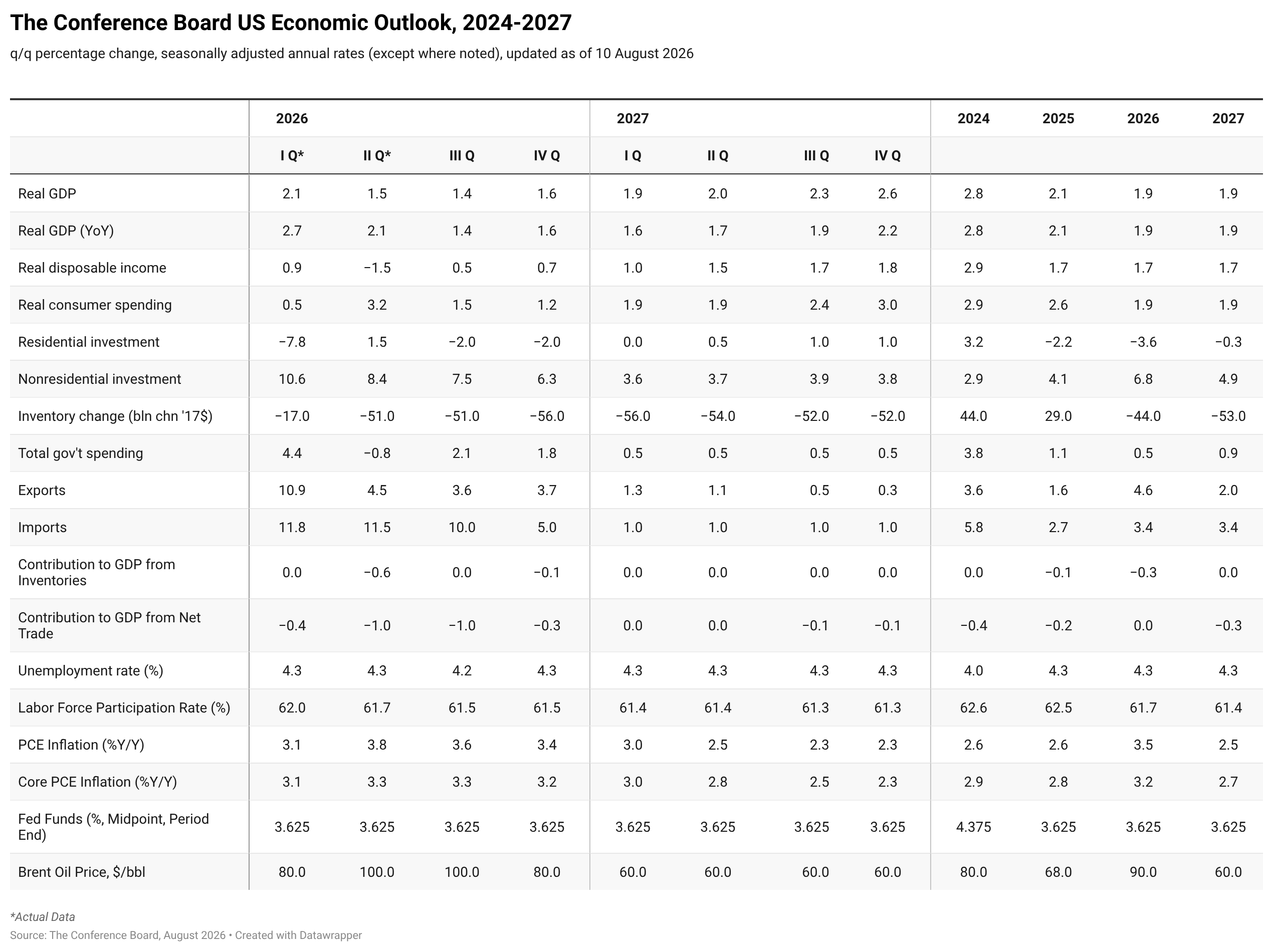

The U.S. economy entered H2 2026 with a more uneven growth profile. One of the defining features of this expansion is the gradual shift toward investment-led growth. Throughout the post-pandemic recovery, household consumption was the primary driver of economic activity. As household affordability becomes increasingly constrained, that leadership is shifting to business investment in productivity-enhancing technologies.U.S. Outlook: Investment Carries Growth as Consumer Affordability Bites

At the macro level, productivity gains from AI are apparent in GDP and in productivity defined by non-farm business output divided by aggregate hours worked. However, for companies and workers, the magnitude of the productivity gains generated by this investment remains uncertain. Still, the growth transition should allow the economy to continue expanding despite softer consumer spending, although the resulting growth profile is likely to remain uneven across industries.

Official data indicate that inflation has moderated, although households continue to face elevated living costs. Inflation has improved, but affordability has not. Consumers continue to face substantially higher living costs than prior to the pandemic due to elevated prices. Housing expenses remain high, homeowner insurance premiums continue to rise rapidly in many parts of the country, financing costs remain restrictive, and cumulative inflation has permanently raised the cost of many essential goods and se

myTCB® Members get exclusive access to webcasts, publications, data and analysis, plus discounts to events.

Charts

The Gray Swans Tool helps C-suite executives better navigate today’s quickly developing economic, political, and technological environments.

LEARN MORECharts

Preliminary PMI indices show no change in weak DM growth momentum in November

LEARN MORE

Charts

How Might the World Fall Back into Recession?

LEARN MORECharts

Passing increases downstream, cutting costs, and absorbing price increases into profit margins are the chief ways to manage rising input costs. Few see changing

LEARN MORECharts

US continues to lead global productivity race

LEARN MORECharts

The Global Economic Fallout of the Ukraine Invasion

LEARN MORECharts

The global supply chain disruption associated with the COVID-19 pandemic has resulted in production delays, shortages, and a spike in inflation in world.

LEARN MORECharts

The Conference Board recently released its updated 2022 Global Economic Outlook.

LEARN MORE

Connect and be informed about this topic through webcasts, virtual events and conferences

PRESS RELEASE

LEI for Spain Rose Again in June

August 07, 2026

PRESS RELEASE

CEO Confidence Increased in Q3 2026

August 06, 2026

PRESS RELEASE

LEI for South Korea Increased Again in June

August 06, 2026

PRESS RELEASE

The Global LEI Fell Slightly Both in May and in the Advanced Estimate for June

July 30, 2026

PRESS RELEASE

US Consumer Confidence Edged Down in July

July 28, 2026

PRESS RELEASE

LEI for China Ticked Up in June

July 23, 2026

All release times displayed are Eastern Time

This report identifies trends to help businesses prepare for an environment with more challenges for labor and capital but improvements in productivity growth.

LEARN MOREConnect and be informed about this topic through webcasts, virtual events and conferences

The Conference Board Economic Forecast for the US Economy

August 10, 2026 | Report

No Signs of Wage Inflation; Labor Market Remains Stable

August 07, 2026 | Brief

Q2 GDP and June Inflation Support September Fed Hold

July 30, 2026 | Brief

FOMC Decision: Hawkish Rhetoric, No Action: September Hike Odds Decline

July 29, 2026 | Brief

July FOMC Preview: Patience Meets Division: The Warsh Fed Faces Its First Test

July 28, 2026 | Brief

July 16, 2026 | Report

USMCA 2.0—Trade Uncertainty in North America

June 10, 2026

Power Shifts: From the Fed to EV Markets

May 13, 2026

The Iran Conflict: Risks for the Global Economy

April 15, 2026

Priced Out: The State of US Housing Affordability

February 11, 2026

The CEO Outlook for 2026—Uncertainty, Risks, Growth & Strategy

January 15, 2026

The Big Picture: What's Ahead for the Global Economy?

December 10, 2025