The Consumer Confidence Survey® reflects prevailing business conditions and likely developments for the months ahead. This monthly report details consumer attitudes, buying intentions, vacation plans, and consumer expectations for inflation, stock prices, and interest rates. Data are available by age, income, 9 regions, and top 8 states.

US Consumer Confidence Plunged Again in April

Latest Press Release

Updated: Tuesday, April 29, 2025

Consumers’ expectations for the future are at a 13-year low

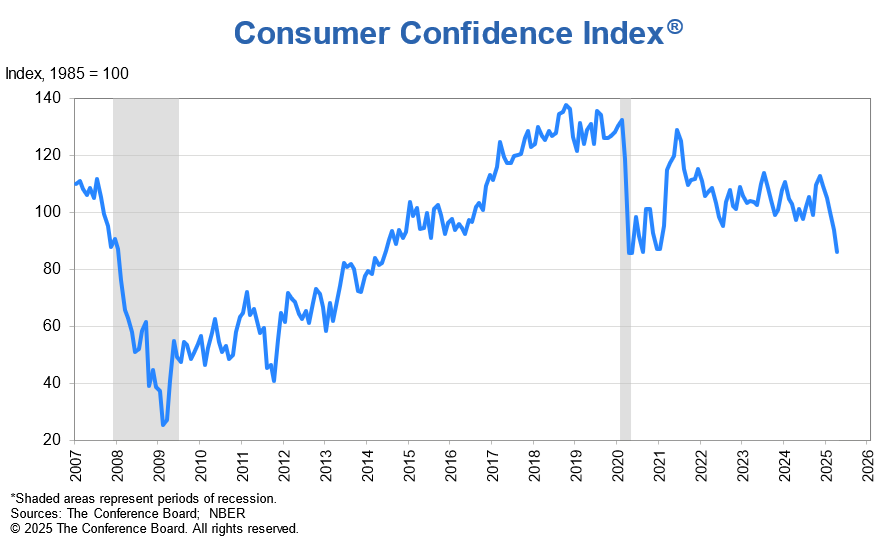

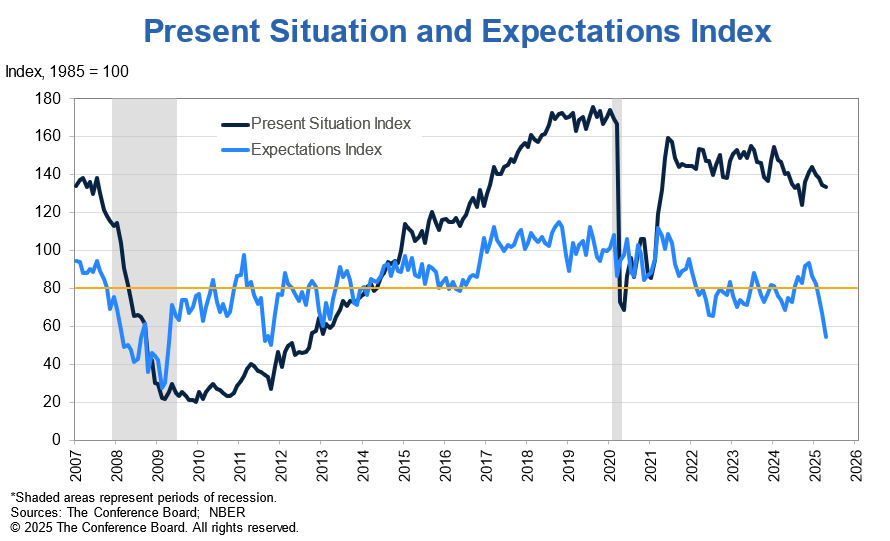

The Conference Board Consumer Confidence Index® fell by 7.9 points in April to 86.0 (1985=100). The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—decreased 0.9 points to 133.5. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—dropped 12.5 points to 54.4, the lowest level since October 2011 and well below the threshold of 80 that usually signals a recession ahead. The cutoff date for preliminary results was April 21, 2025.

“Consumer confidence declined for a fifth consecutive month in April, falling to levels not seen since the onset of the COVID pandemic,” said Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board. “The decline was largely driven by consumers’ expectations. The three expectation components—business conditions, employment prospects, and future income—all deteriorated sharply, reflecting pervasive pessimism about the future. Notably, the share of consumers expecting fewer jobs in the next six months (32.1%) was nearly as high as in April 2009, in the middle of the Great Recession. In addition, expectations about future income prospects turned clearly negative for the first time in five years, suggesting that concerns about the economy have now spread to consumers worrying about their own personal situations. However, consumers’ views of the present have held up, containing the overall decline in the Index.”

April’s fall in confidence was broad-based across all age groups and most income groups. The decline was sharpest among consumers between 35 and 55 years old, and consumers in households earning more than $125,000 a year. The decline in confidence was shared across all political affiliations.

Guichard added: “High financial market volatility in April pushed consumers’ views about the stock market deeper into negative territory, with 48.5% expecting stock prices to decline over the next 12 months (the highest share since October 2011). Meanwhile, average 12-month inflation expectations reached 7% in April—the highest since November 2022, when the US was experiencing extremely high inflation.”

Write-in responses on what topics are affecting views of the economy revealed that tariffs are now on top of consumers’ minds, with mentions of tariffs reaching an all-time high. Consumers explicitly mentioned concerns about tariffs increasing prices and having negative impacts on the economy. Inflation and high prices remained important for consumers’ views about the economy: while the majority complained about the high cost of living, there were also some references to declines in the prices of gas and some food items. There were also numerous mentions of stock prices and uncertainty.

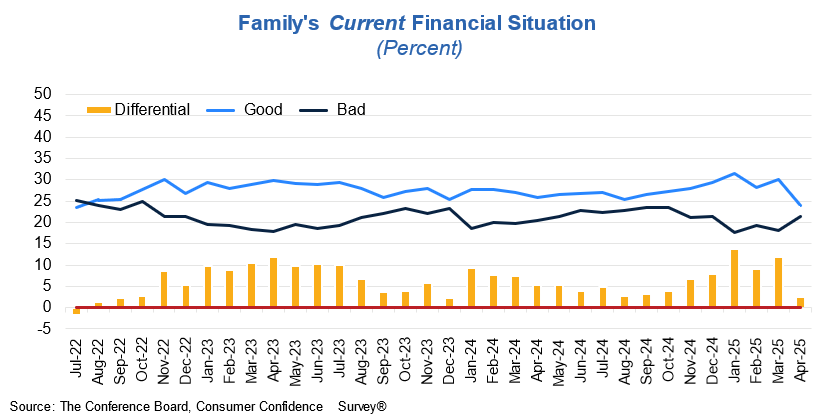

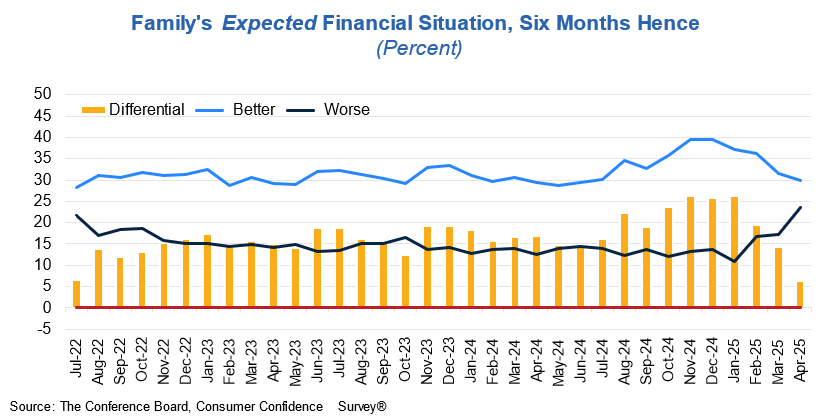

Consumers’ views of their Family’s Current and Future Financial Situations remained in positive territory but weakened substantially. The proportion of consumers anticipating a recession over the next 12 months rose to a two-year high. (These measures are not included in calculating the Consumer Confidence Index®). The share of consumers expecting higher interest rates over the next 12 months continued to increase while the share of consumers expecting lower interest rates dropped further.

On a six-month moving average basis, purchasing plans for both homes and cars declined, as did vacation intentions. Plans to buy big-ticket items—including appliances and electronics—pulled back in April but were mostly up on a 6-month moving average basis. Consumers’ overall intentions to purchase more services in the months ahead were down, with almost all services categories affected. While dining out remained number one among spending intentions, the share of consumers planning to spend more on dining out in the months ahead registered one of the largest month-on-month declines on record in April.

Present Situation

Consumers’ assessments of current business conditions were more positive in April.

- 19.2% of consumers said business conditions were “good,” up from 18.3% in March.

- 16.1% said business conditions were “bad,” down from 16.5%.

Consumers’ views of the labor market weakened in April.

- 31.7% of consumers said jobs were “plentiful,” down from 33.6% in March.

- 16.6% of consumers said jobs were “hard to get,” up from 16.1%.

Expectations Six Months Hence

Consumers’ outlook for business conditions fell further in April.

- 15.7% of consumers expected business conditions to improve, down from 17.8% in March.

- 34.8% expected business conditions to worsen, up from 26.1%.

Consumers’ outlook for the labor market outlook also worsened in April.

- 13.7% of consumers expected more jobs to be available, down from 16.7% in March.

- 32.1% anticipated fewer jobs, up from 28.8%.

Consumers turned negative about their income prospects in April.

- 15.0% of consumers expected their incomes to increase, down from 17.1% in March.

- 18.2% expected their income to decrease, up from 14.9%.

Assessment of Family Finances and Recession Risk

- Consumers’ assessments of their Family’s Current Financial Situation deteriorated in April.

- Consumers’ assessments of their Family’s Expected Financial Situation declined to the lowest level since the question was first asked in 2022.

- Consumers’ Perceived Likelihood of a US Recession over the Next 12 Months increased in April.

The monthly Consumer Confidence Survey®, based on an online sample, is conducted for The Conference Board by Toluna, a technology company that delivers real-time consumer insights and market research through its innovative technology, expertise, and panel of over 36 million consumers. The cutoff date for the preliminary results was April 21.

Source: April 2025 Consumer Confidence Survey®

The Conference Board

The Conference Board publishes the Consumer Confidence Index® at 10 a.m. ET on the last Tuesday of every month. Subscription information and the technical notes to this series are available on The Conference Board website: https://www.conference-board.org/data/consumerdata.cfm.

About The Conference Board

The Conference Board is the member-driven think tank that delivers Trusted Insights for What’s Ahead®. Founded in 1916, we are a non-partisan, not-for-profit entity holding 501 (c) (3) tax-exempt status in the United States. ConferenceBoard.org.

The next release is Tuesday, May 27th at 10 AM ET.

© The Conference Board 2025. All data contained in this table are protected by United States and international copyright laws. The data displayed are provided for informational purposes only and may only be accessed, reviewed, and/or used in accordance with, and the permission of, The Conference Board consistent with a subscriber or license agreement and the Terms of Use displayed on our website at www.conference-board.org. The data and analysis contained herein may not be used, redistributed, published, or posted by any means without express written permission from The Conference Board.

COPYRIGHT TERMS OF USE All material on Our Sites are protected by United States and international copyright laws. You must abide by all copyright notices and restrictions contained in Our Sites. You may not reproduce, distribute (in any form including over any local area or other network or service), display, perform, create derivative works of, sell, license, extract for use in a database, or otherwise use any materials (including computer programs and other code) on Our Sites ("Site Material"), except that you may download Site Material in the form of one machine readable copy that you will use only for personal, noncommercial purposes, and only if you do not alter Site Material or remove any trademark, copyright or other notice displayed on the Site Material. If you are a subscriber to any of the services offered on Our Sites, you may be permitted to use Site Material, according to the terms of your subscription agreement.

Trademarks "THE CONFERENCE BOARD," the TORCH LOGO, "CONSUMER CONFIDENCE SURVEY", "CONSUMER CONFIDENCE INDEX", and other logos, indicia and trademarks featured on Our Sites are trademarks owned by The Conference Board, Inc. in the United States and other countries ("Our Trademarks").

You may not use Our Trademarks in connection with any product or service that does not belong to us nor in any manner that is likely to cause confusion among users about whether The Conference Board is the source, sponsor, or endorser of the product or service, nor in any manner that disparages or discredits us.