Loading...

14 February 2022 / Article

The 2021 proxy season was unprecedented, but the 2022 proxy season is likely to be even more contentious. Expect a greater number of environmental and social (E&S) shareholder proposals to be submitted and more of them to go to a vote with greater support. With the prospect of additional SEC disclosure rules on climate change, human capital management (HCM), and other environmental, social & governance (ESG) topics, shareholders are likely to stake out and hold firm to their positions on proposals relating to ESG reporting. Compromise is still possible, but negotiating the withdrawal of a proposal will likely be hardest to achieve on topics such as lobbying, say-on-climate, gender/racial pay gaps, and racial equity/civil rights audits (included in the human rights category of proposals in the heat map below).

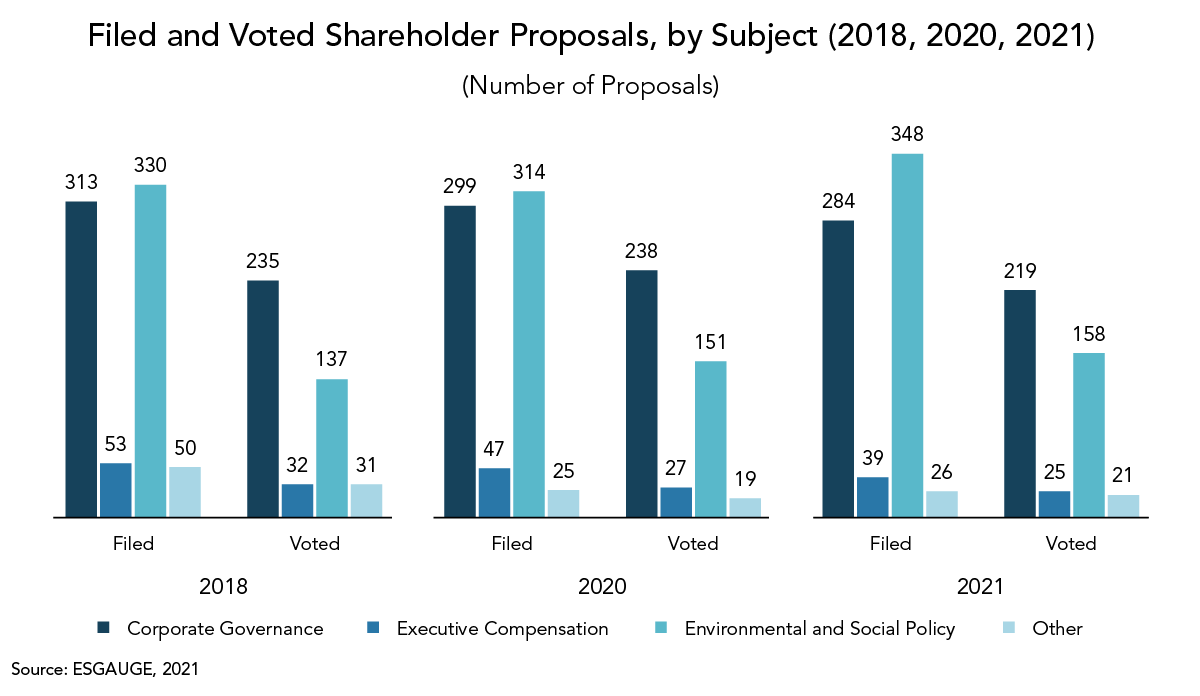

Fueled by a rise in “S” proposals on topics such as diversity and corporate purpose, the number of E&S proposals increased significantly in 2021.1,2 In the Russell 3000, during the first half of 2021, shareholders filed 348 E&S proposals and voted on 158 of them, compared to 314 filed and 151 voted proposals in the first half of 2020. While the number of E&S proposals grew, the number of filed and voted governance proposals (284 and 219, respectively) and executive compensation proposals (39 and 25, respectively) declined compared to 2020.

E&S proposals received unprecedented support in 2021, with some proposals receiving majority support for the first time. Support for E&S (including HCM) proposals averaged 32 percent (compared with 28 percent in 2020 a

myTCB® Members get exclusive access to webcasts, publications, data and analysis, plus discounts to events.