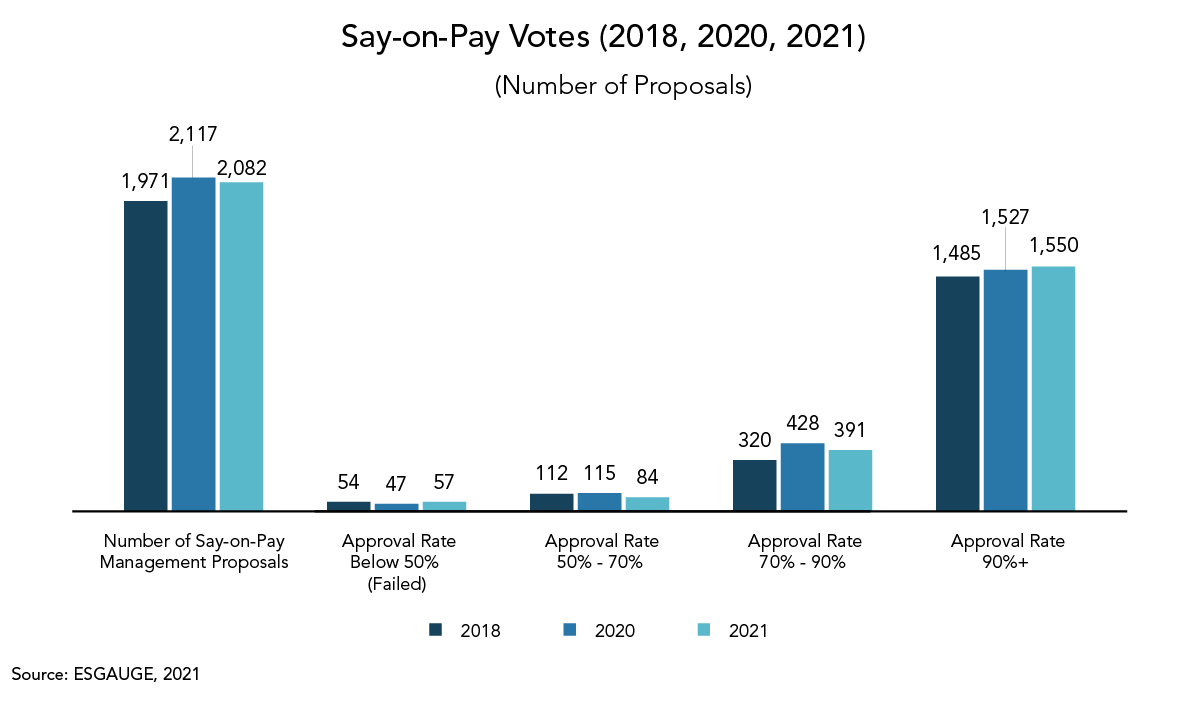

Yet even though the number of failed say-on-pay votes was higher in 2021 than in 2020, more companies (in absolute and relative terms) received at least 90 percent support (1,550 companies, or 74 percent, in 2021 versus 1,527 companies, or 72 percent, in 2020). Additionally, 84 companies (or 4 percent) failed to reach at least 70 percent support in 2021 (a decline from the 115 companies, or 5.4 percent, found in 2020)—the threshold below which proxy advisors begin to scrutinize companies’ responsiveness to shareholder concerns.

Overall, the high support level suggests that investors generally approved the pay decisions companies made in response to the COVID-19 pandemic—except at the largest companies. Companies with an annual revenue of $50 billion and over, whose total CEO compensation packages are the largest on average,2 performed the worst, relatively speaking: only 48 percent of such companies received at least 90 percent support, 10 percent failed to reach at least 70 percent, and 18 percent failed to receive majority support altogether—a sign that the largest companies continue to face the most investor scrutiny of their pay practices. (Companies in the financial and real estate sectors are not part of this analysis.)

|

2021

|

Number of Proposals

|

90%+

|

Below 50% (Failed)

|

|

Annual Revenue

|

n=1,503

|

|

|

|

Under $100 million

|

167

|

57%

|

3%

|

|

$100-999 million

|

443

|

79%

|

2%

|

|

$1-4.9 billion

|

539

|

79%

|

3%

|

|

$5-9.9 billion

|

143

|

74%

|

4%

|

|

$10-24.9 billion

|

141

|

70%

|

3%

|

|

$25-49.9 billion

|

30

|

70%

|

0%

|

|

$50 billion and over

|

40

|

48%

|

18%

|

Expect the number of companies receiving a negative say-on-pay vote to increase, especially at the largest companies and at companies that don’t provide sufficient context and detail on executive compensation decisions.

How CEOs and boards can maintain support for say-on-pay proposals

The level of total executive compensation for the largest companies, as well as concerns about how companies addressed performance share units (PSUs) during the COVID-19 pandemic (including changes to “in-flight” PSU programs [programs whose performance measurement period is still ongoing] and additional PSU grants), caused heightened investor scrutiny at those companies. Even though investors advocated for PSU programs over the use of restricted stock and stock options, they have concerns about how those programs have been structured and implemented. Investors sometimes find that performance goals set by the compensation committee are too easy to meet, that the committee approves unwarranted adjustments that bring the payout to target or above, or that there’s still a disconnect between payouts and the company’s stock performance.3 Those concerns were exacerbated at companies that took actions to reduce the impact of the pandemic on payouts under existing the PSU programs.

Compensation committees, especially at the largest companies, may want to consider:

- Keeping the executive compensation plan simple so it can be understood by investors—and the executives it is intended to motivate.

- Setting the performance threshold for a minimum payout at a level that gives executives the chance for an earnout even when the company has a bad year but sets a high bar for a maximum payout to drive superior performance.

- Reintroducing relative total shareholder return (TSR) or making it a more prominent feature of the executive compensation program as it aligns payouts with shareholder interest.

- Making performance goals relative to peers when possible (although this can be problematic when there isn’t a sufficiently large and comparable peer group).

- Simplifying the “adjustment” process, verifying any adjustments when determining payouts, and avoiding adjusting programs before the performance measurement period has ended.

But most importantly, boards should understand why investors voted against their executive compensation plan—whether shareholders deemed the total compensation excessive, disapproved of the PSU plan, or used the say-on-pay vote to send a message to the board on other, unrelated topics.

Providing thorough context and detail on executive compensation decisions, including adjustments, can help prevent a negative say-on-pay vote. Therefore, the why of the pay plan should be featured prominently in the proxy statement, and supplemental filings can help to tell a company’s specific story. And when it comes to linking executive compensation to ESG performance, the main lesson from the past decades is to proceed with care.4

Director Elections: Opposition Greatest at Smaller Companies

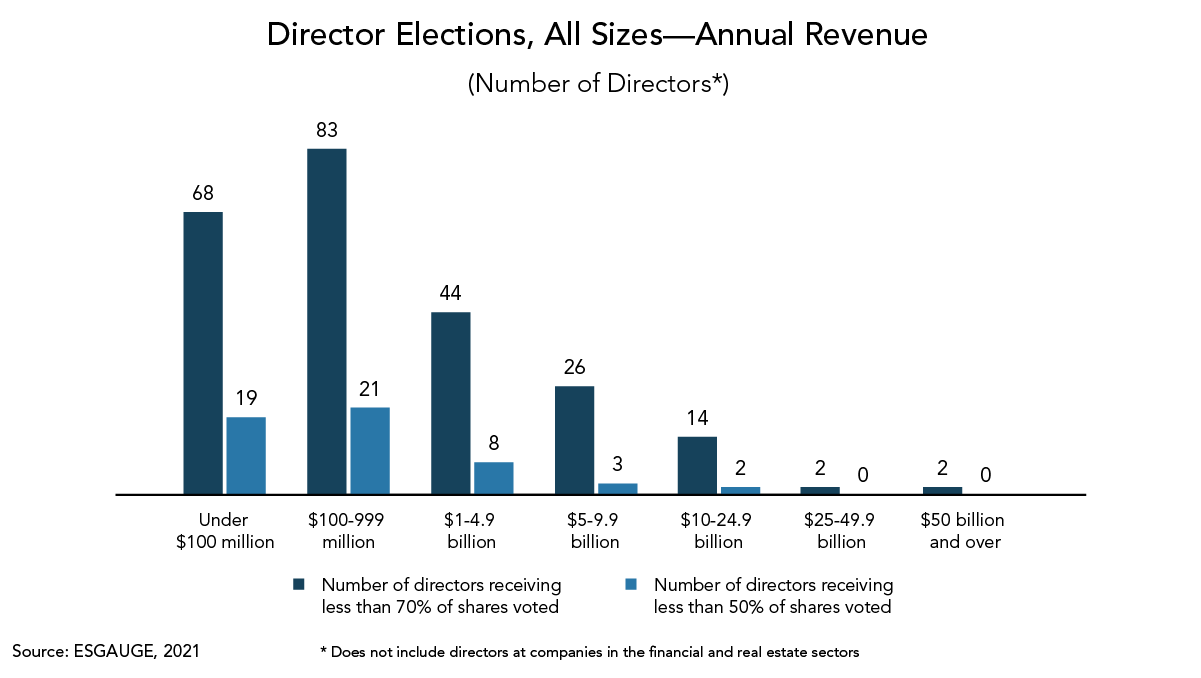

Average support levels in director reelections continued to decline in the first half of 2021. In the Russell 3000, support dropped from 98 percent of votes cast in 2018 to 94.8 percent in 2020 and further down to 94.6 percent in 2021. Moreover, the number of directors failing to receive majority support more than doubled in recent years, from 27 in 2018 to 68 in 2021. And of those 68 directors, 40 (59 percent) were serving on the board of companies with an annual revenue under $1 billion. Similarly, the number of directors receiving between 50 and 70 percent of votes cast rose from 86 in 2018 to 308 in 2021, and of those 308 directors, 151 (almost half) were serving on smaller companies with an annual revenue under $1 billion.

These numbers confirm that shareholders perceive smaller companies to be lagging their bigger counterparts in terms of governance practices, including board composition and refreshment, and oversight of ESG issues. Consequently, they face major investor scrutiny. This trend is expected to continue in 2022, as proxy advisors and investors have updated their proxy voting guidelines and policies for 2022 to hold directors accountable for what they see as ESG oversight failures.

How CEOs and boards can avoid growing opposition to director elections

Directors increasingly realize that ESG risks and opportunities affect a company’s ability to create long-term value and that being unresponsive can have an impact not only on director elections but on shareholder activism with a big “A.” Therefore, it is pivotal for boards to have oversight of, and demonstrate fluency in, ESG. Boards will want to:

- Assess board composition and structure to ensure they have the appropriate board- and board committee-level oversight of the company’s key ESG risks and opportunities.5 The allocation of oversight responsibilities among board committees will vary by company, but it’s important not to overload the audit committee. While that committee often has overall responsibility for risk management (requiring audit committees to discuss policies with respect to risk assessment and risk management), other existing committees (or perhaps new committees) may be better able to focus on specific ESG matters.6

- Involve one or more board members in all their engagements with their shareholders to demonstrate they are conversant in ESG. There seems to be a constant requirement for boards to add new members with specialized expertise on topics from cybersecurity to sustainability. But although it’s harder to convey through disclosures, collective board fluency in ESG is much more important than narrow expertise.

Growing Retail Investor Base Is Affecting Voting Dynamic

With the top 10 institutional investors holding 30 percent of the S&P 500, and with ESG funds predicted to grow from $8 trillion today to $30 trillion by the end of this decade, the push on ESG will continue to come mainly from institutional investors.7

Yet, with the changing dynamics in the composition, views, and impact of their retail investor base, companies should also consider new, cost-effective ways of reaching this fast-growing investor category. Propelled by the pandemic as well as the rise of trading apps, retail trading is booming, and a new generation of retail investors is becoming increasingly influential. But these investors don't always have the same focus as their institutional counterparts and companies can't engage with them in the traditional way. Since retail investors tend to be less involved in proxy voting (they often don’t understand what their vote will do or what shareholder proposals are asking for), several companies had trouble reaching quorum in 2021. A retail-facing strategy can promote retail investors’ participation in the proxy voting process. To get more participation, companies will want to:

- Gain access to retail investor data (e.g., from a shareholder data services provider) to better understand 1) who their retail investors are; 2) what their sentiment and voting behavior is on key issues; and 3) where and how they can best engage and educate them on ESG issues (e.g., on social media or digital trading platforms, online finance communities, or through retail investor events), as well as try to change any negative sentiment.

**********

This brief is part of a suite of seven reports: 2022 Proxy Season Preview and Shareholder Voting Trends (2018-2021). Visit conferenceboard.esgauge.org/shareholdervoting to access and manipulate our data online.

[1] The data and figures in this report and all six supplemental briefs represent shareholder proposals submitted at Russell 3000 companies in the first half of 2021, 2020, and 2018. About 90 percent of shareholder meetings at Russell 3000 companies take place in the first half of the year, and this cutoff point also allows easy comparisons with our prior-year shareholder voting benchmarking reports.