The Consumer Confidence Survey® reflects prevailing business conditions and likely developments for the months ahead. This monthly report details consumer attitudes, buying intentions, vacation plans, and consumer expectations for inflation, stock prices, and interest rates. Data are available by age, income, 9 regions, and top 8 states.

US Consumer Confidence Inched Up Again in March

Latest Press Release

Updated: Tuesday, March 31, 2026

Surging costs from tariffs and war notwithstanding, Confidence edged higher

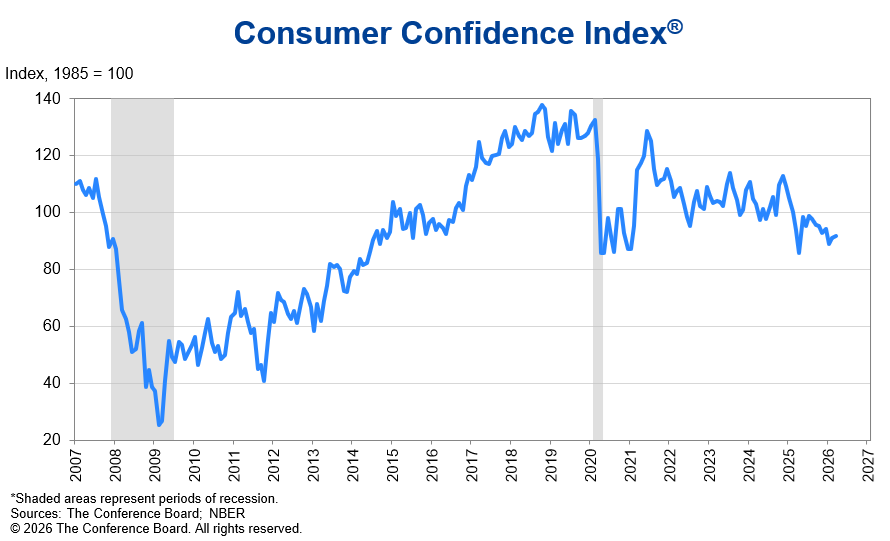

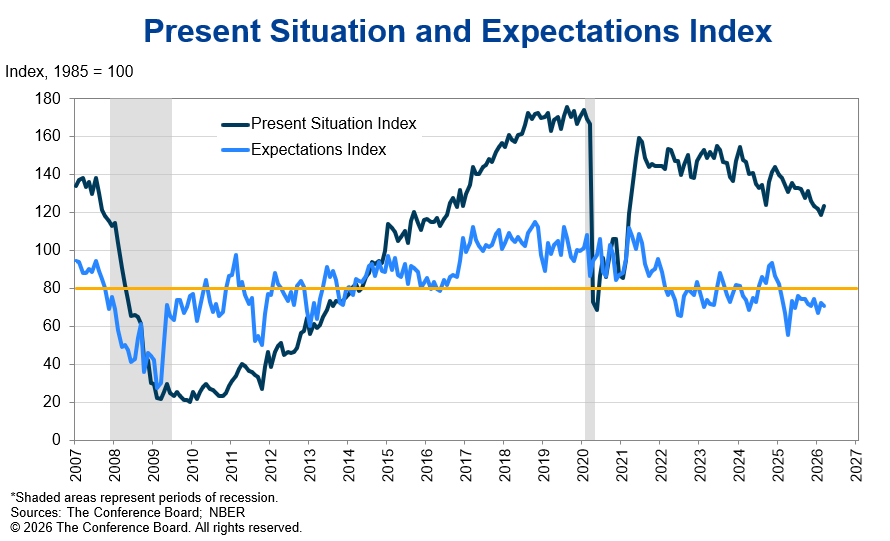

The Conference Board Consumer Confidence Index® edged up by 0.8 points in March to 91.8 (1985=100), from 91.0 in February. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—increased by 4.6 points to 123.3. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—declined by 1.7 points to 70.9. The survey period for preliminary results was March 1 to 24, 2026. While not obvious in the headline or its component indexes, the weight of rising costs due to tariff passthrough and spiking oil prices was evident among other measures in the survey like inflation expectations.

“Consumer confidence ticked up again in March, as a modest improvement in consumers’ views of current conditions outweighed a slight downshift in expectations for the future,” said Dana M Peterson, Chief Economist, The Conference Board. “Three of five components of the Index firmed in March, and overall confidence improved modestly for a second month. Nonetheless, the Index has been on a general downward trend since 2021.”

The Present Situation Index rose again in March, as net views of current business conditions rose to +5.6% after hovering around 1-2% for three months. Perceptions of employment conditions improved slightly, with the labor market differential—the share of consumers saying jobs are “plentiful” minus the share saying jobs are “hard to get”—ticking up by 0.1 ppt to +5.8%. The Expectations Index dipped as two of three components—net perceptions of labor market and household income conditions six months from now—edged downward. However, expected business conditions were slightly less pessimistic in March.

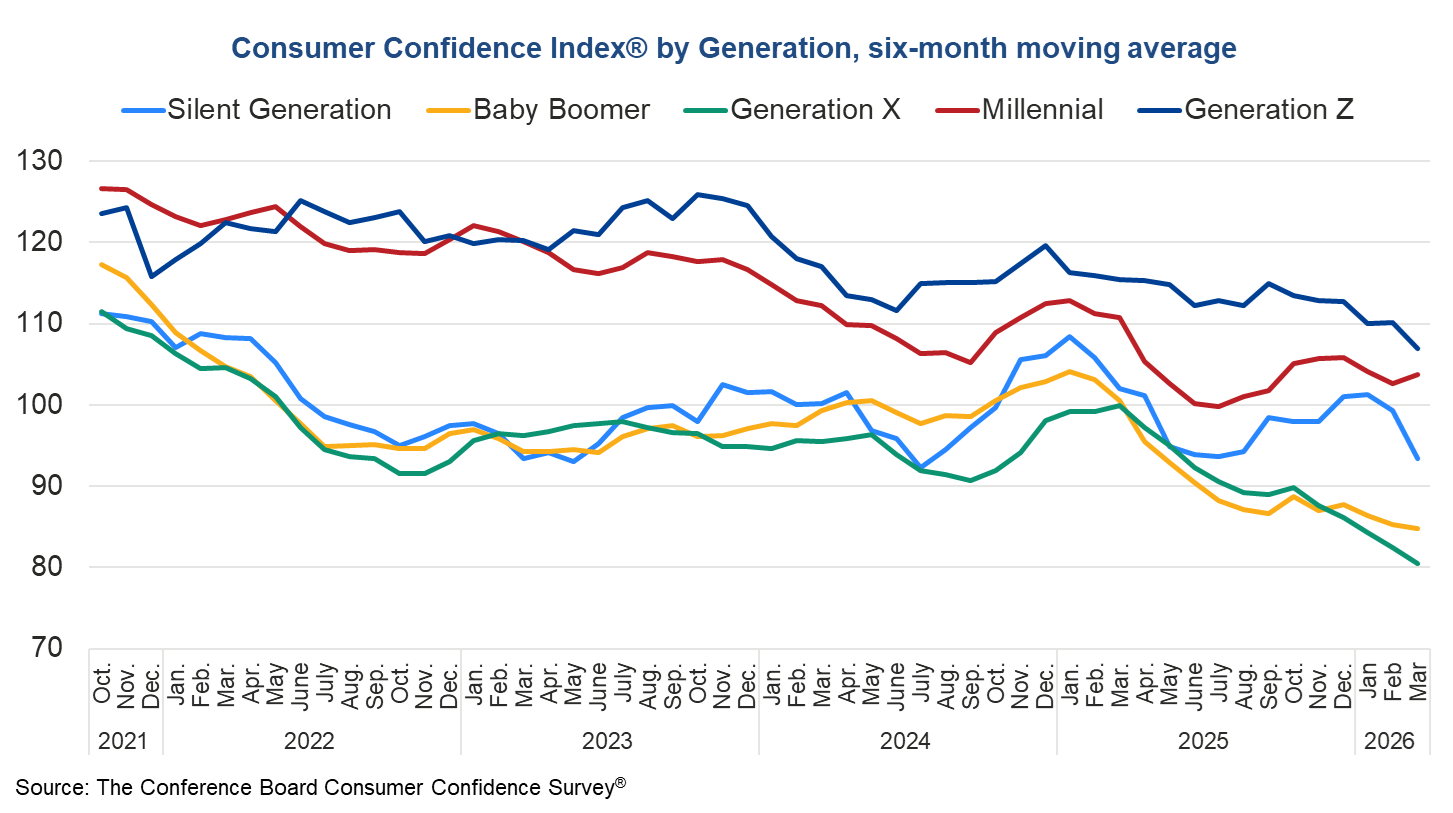

Among demographic groups, confidence on a six-month moving average basis continued to moderate in March for consumers under age 35 and 55 and over, and virtually unchanged after a multi-month decline for those aged 35 to 54. Respondents under 35 remain the most optimistic and those 55 and over the least. On a six-month moving average basis, Generation Z remained the most confident among all generations, but their optimism slipped in March along with the Silent Generation, Baby Boomers, and Generation X. Only Millennials cited improved confidence in the month. By income, confidence on a six-month moving average basis continued to dip in six of eight income groups. Only consumers earning $25,000-34,999 and $125,000 and over were somewhat more optimistic. Consumer confidence by political affiliation was little changed. Republicans remained the most optimistic, while confidence was substantially lower among Independents and the lowest among Democrats.

Peterson added: “Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism. Comments about prices and the cost of goods suggest that the cost of living remained at the top of consumers’ minds. As the war in Iran overlapped significantly with the survey sample period, comments about oil/gas and war/conflict spiked, while specific mentions of trade and tariffs decreased notably.”

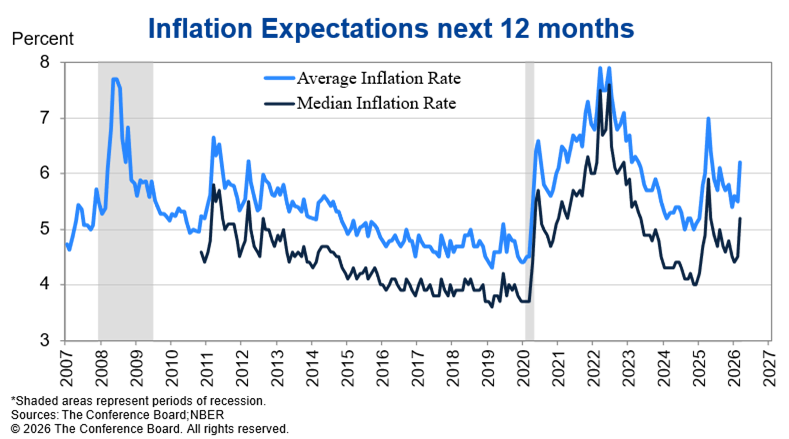

Unsurprisingly given the Iran war oil shock, consumers’ average and median 12-month inflation expectations surged in March to levels last seen in August 2025, when US consumers awaited more tariff announcements from the US federal government. Consequently, the percentage of consumers stating that interest rates over the next 12 months will be higher on net skyrocketed from 34.9% to 42.4%. Expectations for higher stock prices a year from now plunged.

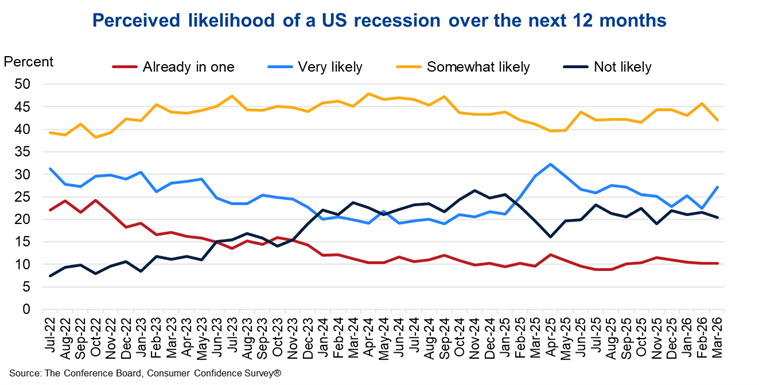

Consumers’ net views of their Family’s Current Financial Situation improved slightly in March after a February retreat. Expectations for their Family’s Future Financial Situation continued to be less optimistic. Meanwhile, the share of consumers who said a US recession over the next 12 months is “very likely” rose, while those saying “somewhat likely” or “not likely” fell. The cohort believing the US is already in a recession was virtually unchanged. (These measures are not included in calculating the Consumer Confidence Index®).

Consumers’ plans to buy big-ticket items over the next six months shifted from “yes” and “maybe” in February, to “no” in March. Nonetheless, the proportion saying “yes” remained well above the other responses. Used cars, furniture, TVs, and smartphones remained the most popular items within their respective categories for future purchases. Among all expensive items, furniture persists as the top expected purchase.

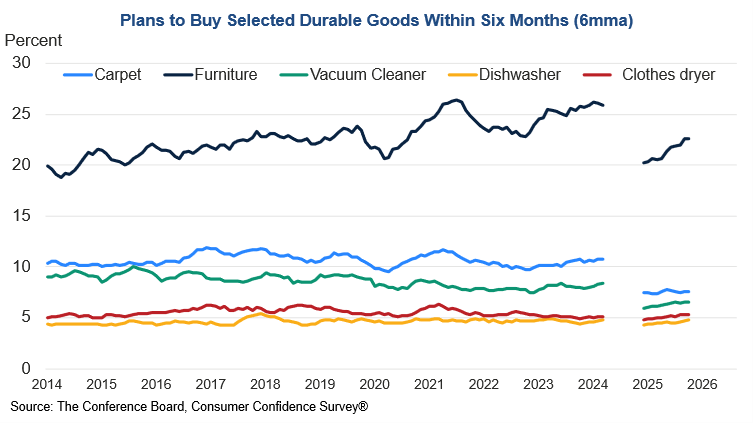

Buying plans for autos continued rising on a six-month moving average basis in March, with used cars remaining the clear preference over new cars. Homebuying expectations were somewhat lower on a six-month rolling basis for both existing and new units in the month, with consumers continuing to prefer existing homes to newly built ones. Purchase plans for all types of home furnishings, white goods, and electronics on a six-month moving average basis improved in March.

Consumers planning more spending on services over the next six months also shifted from “yes” and “maybe” to “no.” Consumer spending trends in 2026 remain focused on “cheap thrills” and necessary services, and away from expensive and highly discretionary activities.

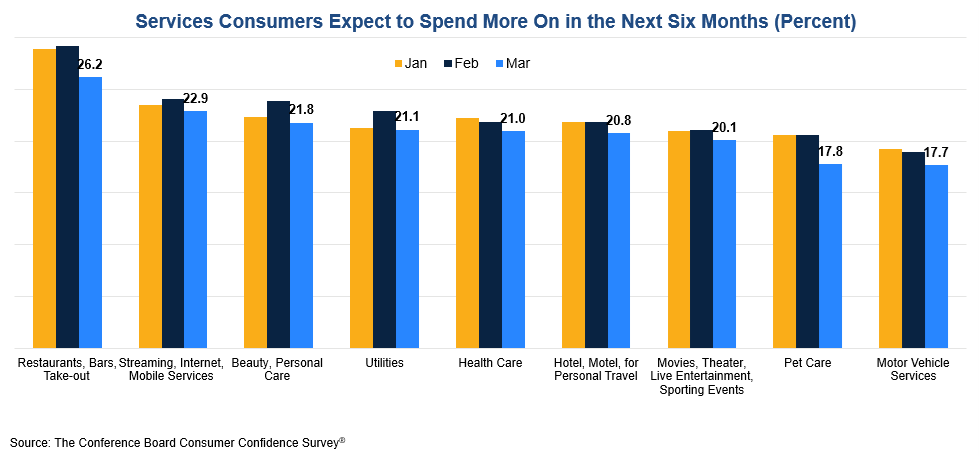

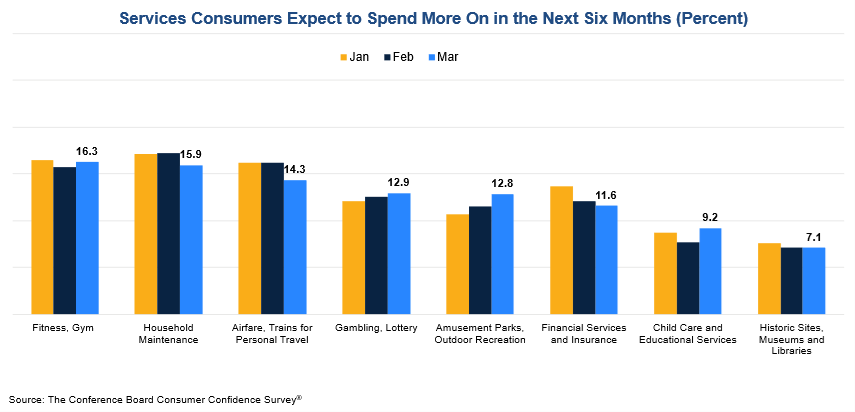

Among services, anticipated spending over the next six months fell for every category in March, except for fitness/gym, gambling/lottery, amusement park/outdoor recreation, and childcare/education. Despite dipping in the month, restaurants/bars/take-out remained the top category for expected spending ahead, still followed by streaming/internet/mobile services and beauty and personal care. However, utilities and healthcare displaced hotel/motel for personal travel among the top five future spending categories. This displacement is consistent with the dip in overall vacation plans over the next six months, and consumers’ continued complaints about rising electricity and healthcare costs. Domestic travel intentions remained buoyant in March, but foreign travel plans collapsed, likely due to conflicts abroad. Expected spending on airfare/trains for personal travel fell in March after being unchanged from January to February.

Present Situation

Consumers’ views of current business conditions improved in March.

- 21.9% of consumers said business conditions were “good,” up from 20.4% in February.

- 16.3% said business conditions were “bad,” down from 19.0%.

On net, consumers’ views of the labor market were virtually unchanged in March.

- 27.3% of consumers said jobs were “plentiful,” up slightly from 26.7% in February.

- 21.5% of consumers said jobs were “hard to get,” also up slightly from 21.0%.

Expectations Six Months Hence

Consumers were a tad less pessimistic about future business conditions in March.

- 18.2% of consumers expected business conditions to improve, up from 17.6% in February.

- 21.3% expected business conditions to worsen, a small uptick from 21.2%.

However, consumers were more negative about the labor market outlook in March.

- 15.4% of consumers expected more jobs to be available, down from 16.0% in February.

- 27.9% anticipated fewer jobs, up from 26.2%.

Consumers’ outlook for their income prospects was slightly less optimistic in March.

- 19.2% of consumers expected their incomes to increase, up from 18.4% in February.

- 13.9% expected their incomes to decline, up from 12.5%.

The monthly Consumer Confidence Survey®, based on an online sample, is conducted for The Conference Board by Toluna, a technology company that delivers real-time consumer insights and market research through its innovative technology, expertise, and panel of over 36 million consumers. The cutoff date for the preliminary results was March 24.

Source: March 2026 Consumer Confidence Survey®

The Conference Board

The Conference Board publishes the Consumer Confidence Index® at 10 a.m. ET on the last Tuesday of every month. Subscription information and the technical notes to this series are available on The Conference Board website: https://www.conference-board.org/data/consumerdata.cfm.

About The Conference Board

The Conference Board is the member-driven think tank that delivers Trusted Insights for What’s Ahead®®. Founded in 1916, we are a non-partisan, not-for-profit entity holding 501 (c) (3) tax-exempt status in the United States. TCB.org

The next release is Tuesday, April 28 at 10 AM ET.

© The Conference Board 2026. All data contained in this table are protected by United States and international copyright laws. The data displayed are provided for informational purposes only and may only be accessed, reviewed, and/or used in accordance with, and the permission of, The Conference Board consistent with a subscriber or license agreement and the Terms of Use displayed on our website at www.conference-board.org. The data and analysis contained herein may not be used, redistributed, published, or posted by any means without express written permission from The Conference Board.

COPYRIGHT TERMS OF USE All material on Our Sites are protected by United States and international copyright laws. You must abide by all copyright notices and restrictions contained in Our Sites. You may not reproduce, distribute (in any form including over any local area or other network or service), display, perform, create derivative works of, sell, license, extract for use in a database, or otherwise use any materials (including computer programs and other code) on Our Sites ("Site Material"), except that you may download Site Material in the form of one machine readable copy that you will use only for personal, noncommercial purposes, and only if you do not alter Site Material or remove any trademark, copyright or other notice displayed on the Site Material. If you are a subscriber to any of the services offered on Our Sites, you may be permitted to use Site Material, according to the terms of your subscription agreement.

Trademarks "THE CONFERENCE BOARD," the TORCH LOGO, "CONSUMER CONFIDENCE SURVEY", "CONSUMER CONFIDENCE INDEX", and other logos, indicia and trademarks featured on Our Sites are trademarks owned by The Conference Board, Inc. in the United States and other countries ("Our Trademarks").

You may not use Our Trademarks in connection with any product or service that does not belong to us nor in any manner that is likely to cause confusion among users about whether The Conference Board is the source, sponsor, or endorser of the product or service, nor in any manner that disparages or discredits us.