The Consumer Confidence Survey® reflects prevailing business conditions and likely developments for the months ahead. This monthly report details consumer attitudes, buying intentions, vacation plans, and consumer expectations for inflation, stock prices, and interest rates. Data are available by age, income, 9 regions, and top 8 states.

US Consumer Confidence Fell Again in December

Latest Press Release

Updated: Tuesday, December 23, 2025

Confidence weakened for a fifth consecutive month as perceptions of business conditions were negative, and apprehensions about jobs and income deepened

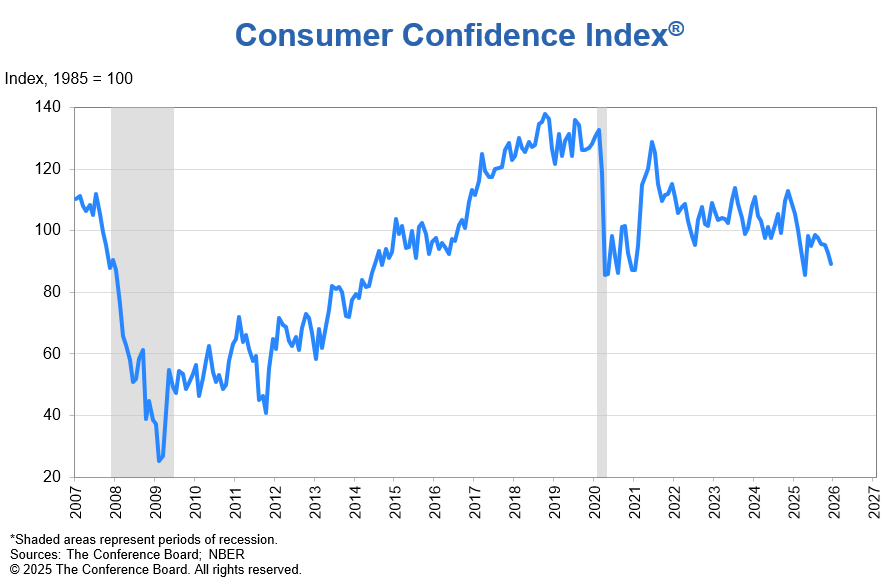

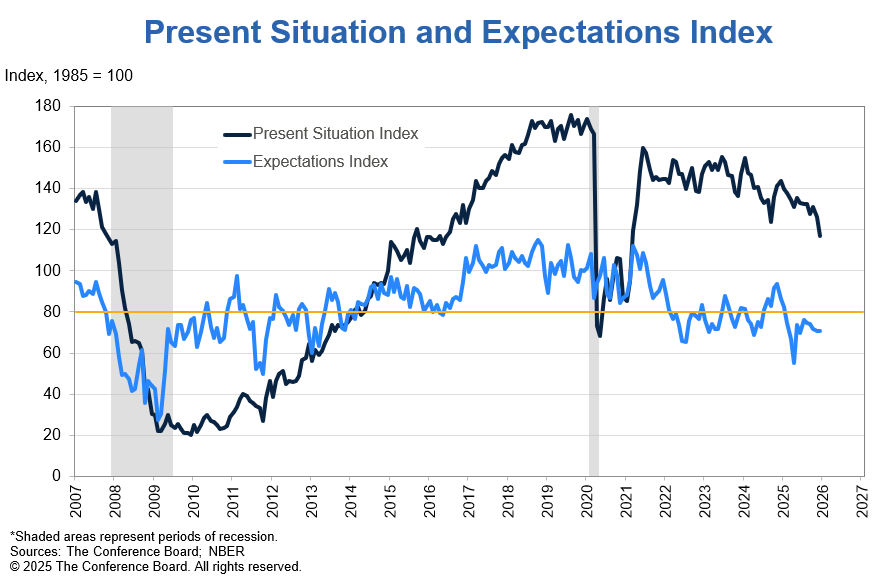

The Conference Board Consumer Confidence Index® declined by 3.8 points in December to 89.1 (1985=100), from 92.9 in November. This includes an upward revision to November’s reading, as responses collected after the end of the federal government shutdown (which spanned October 1 to November 12) were more positive than those collected during the impasse. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—plummeted by 9.5 points to 116.8 in December. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—held steady at 70.7. The Expectations Index has now tracked under 80 for 11 consecutive months, the threshold below which the gauge signals recession ahead. The cutoff for preliminary results was December 16, 2025.

“Despite an upward revision in November related to the end of the shutdown, consumer confidence fell again in December and remained well below this year’s January peak. Four of five components of the overall index fell, while one was at a level signaling notable weakness,” said Dana M Peterson, Chief Economist, The Conference Board.

The Present Situation Index declined as net views on current business conditions were negative for the first time since September 2024, a month that included a labor market scare and deadly hurricanes. Perceptions of employment conditions edged lower as the labor market differential—the share of consumers saying jobs are ‘plentiful’ minus the share saying jobs are ‘hard to get’—continued to flag. Two of the three Expectations Index components dipped in December. November’s nosedive in expectations for business conditions six months from now mostly reversed in December but remained negative. Expectations for labor market conditions were gloomier, and the outlook for household incomes was less positive.

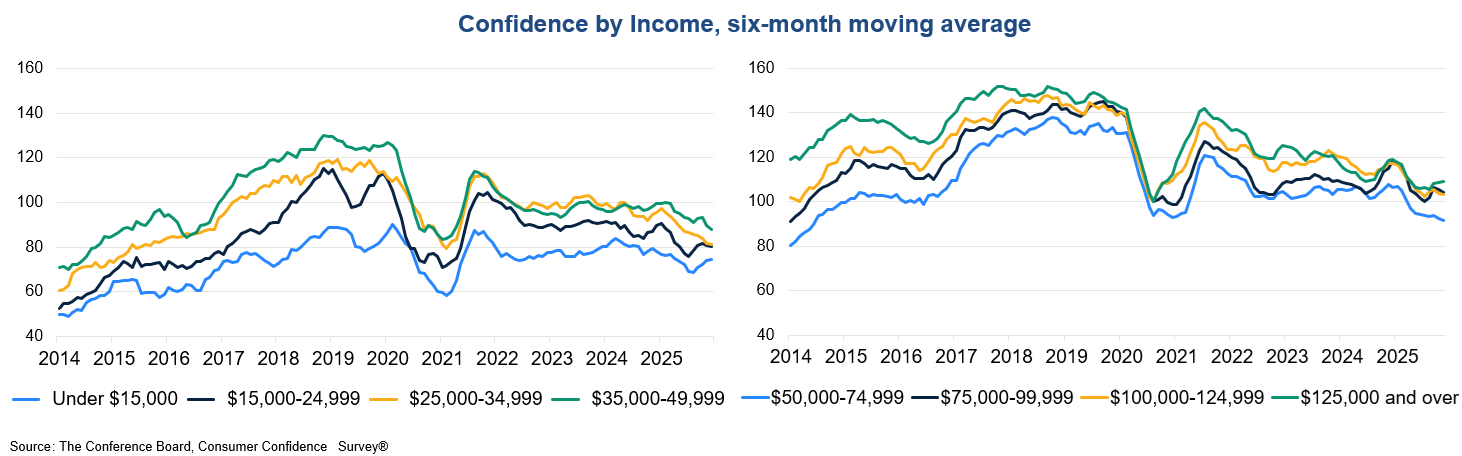

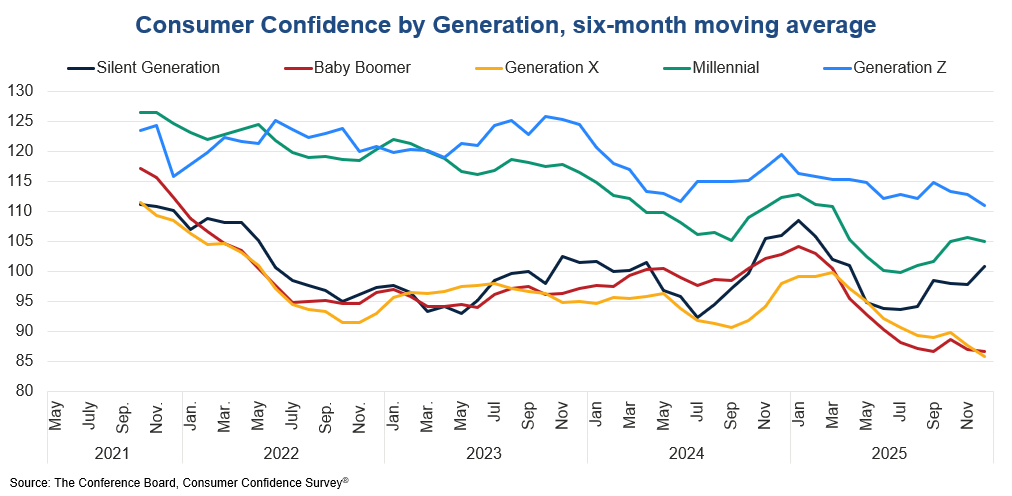

Among demographic groups, on a six-month moving average basis, confidence dipped among all age groups in December, although consumers under 35 continued to be more confident than consumers age 35 and older. There were few generational differences, as confidence among all generations trended downward in the month, with only the Silent Generation becoming more hopeful. Millennials and Gen Z remained the most optimistic of all generations surveyed. By income, confidence on a six-month moving average basis fell for nearly all brackets, except for those earning less than $15K and more than $125K. Still, consumers earning less than $15K remained the least optimistic among all income groups. Confidence continued to fall in December among all political affiliations (Democrats, Republicans, and Independents).

Peterson added: “Consumers’ write-in responses on factors affecting the economy continued to be led by references to prices and inflation, tariffs and trade, and politics. However, December saw increases in mentions of immigration, war, and topics related to personal finances—including interest rates, taxes and income, banks, and insurance. The responses continued to skew pessimistic but less so than November, potentially due to fewer negative comments about prices and inflation, politics, as well as a rebound in positive responses about interest rates. Notably, the Federal Reserve Board cut monetary policy rates on December 10 for a third time in 2025, which landed in the second half of the survey sample interval.”

Nonetheless, the share of consumers expecting interest rates to rise were on net higher, with a drop in the proportion expecting lower rates. Consumers’ median and average 12-month inflation expectations both retreated in December after an uptick in November. The balance of consumers’ expectations for stock prices twelve months from now—higher minus lower—was the most positive since January 2025.

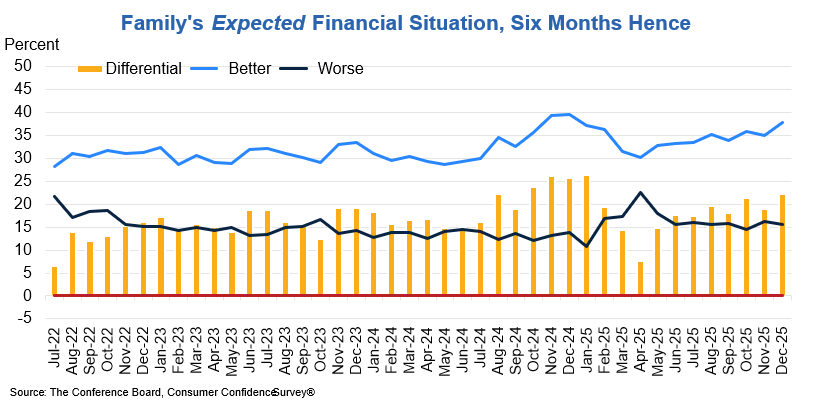

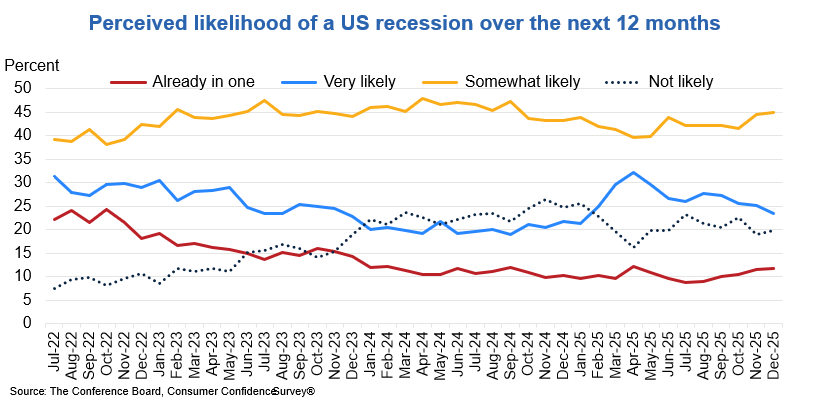

On net, consumers’ views of their Family’s Current Financial Situation collapsed into negative territory for the first time in nearly four years. However, expectations for their Family’s Future Financial Situation were the most positive since January of this year. Meanwhile, the share of consumers believing a US recession over the next 12 months is “not likely” edged up to about one-fifth of respondents and those saying recession is “very likely” continued to recede. Still, the largest share of consumers—those anticipating that recession is “somewhat likely”—grew again and the small percentage stating that the US is “already in one” crept higher. (These measures are not included in calculating the Consumer Confidence Index®).

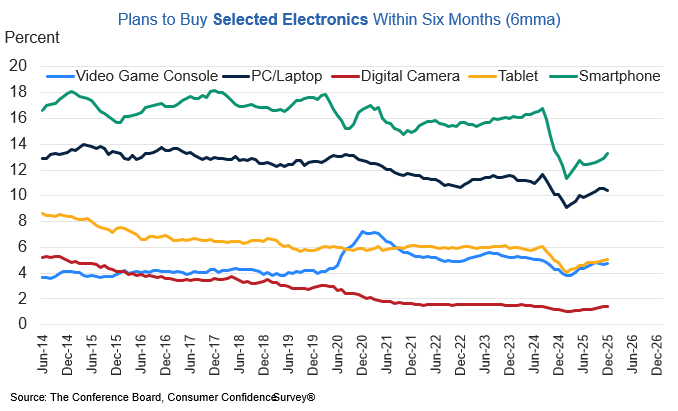

Consumers appeared more cautious about plans for buying big-ticket items over the next six months. Consumers who said “yes” to buying big-ticket items ahead edged higher in December. However, the number of those saying “no” increased and “maybe” declined. Overall buying plans for autos dipped again in December. On a six-month moving average basis, expectations for purchasing new cars continued to slip, but plans to buy used cars continued to climb. Homebuying expectations also ticked downward. Plans to buy household appliances all dipped, as did purchasing plans for PCs and laptops, as well as video game consoles. By contrast, future spending plans for smartphones, tablets, and digital cameras continued to trend upward on a six-month moving average basis. Used cars, TVs, and smartphones remained the most popular within their categories for future purchases.

On balance, consumer spending trends in 2025 moved towards cheap thrills and necessary services and away from expensive and highly discretionary activities. In December, consumers’ planned spending on services over the next six months were little changed from November, but those saying “yes” to buying more services remained healthy. Month-over-month, anticipated spending on restaurants, streaming, personal care, and utilities picked up in December, while future purchases of other discretionary services categories softened. The top categories for planned services spending over the next six months still included restaurants, bars, take-out; streaming, internet, mobile services; beauty and personal care; utilities; and healthcare. Vacation intentions continued to spiral downward in December. Plans for domestic travel over the next six months still exceed international vacation plans, but both types fell.

Present Situation

Consumers’ assessments of current business conditions turned mildly pessimistic in December.

- 18.7% of consumers said business conditions were “good,” down from 21.0% in November.

- 19.1% said business conditions were “bad,” up from 15.8%.

Consumers’ views of the labor market were also weaker in December.

- 26.7% of consumers said jobs were “plentiful,” down from 28.2% in November.

- 20.8% of consumers said jobs were “hard to get,” up from 20.1%.

Expectations Six Months Hence

Consumers were moderately less pessimistic about future business conditions in December.

- 18.0% of consumers expected business conditions to improve, down from 18.1% in November.

- However, 21.8% expected business conditions to worsen, down from 25.8%.

Consumers were on net a bit more worried about the labor market outlook in December

- 16.5% of consumers expected more jobs to be available, unchanged from November.

- 27.4% anticipated fewer jobs, up from 26.8%.

Consumers’ outlook for their income prospects was slightly less positive in December.

- 18.4% of consumers expected their incomes to increase, up from 17.6% in November.

- Meanwhile, 14.7% expected their incomes to decrease, up from 12.5%.

The monthly Consumer Confidence Survey®, based on an online sample, is conducted for The Conference Board by Toluna, a technology company that delivers real-time consumer insights and market research through its innovative technology, expertise, and panel of over 36 million consumers. The cutoff date for the preliminary results was December 16.

Source: December 2025 Consumer Confidence Survey®

The Conference Board

The Conference Board publishes the Consumer Confidence Index® at 10 a.m. ET on the last Tuesday of every month. Subscription information and the technical notes to this series are available on The Conference Board website: https://www.conference-board.org/data/consumerdata.cfm.

About The Conference Board

The Conference Board is the member-driven think tank that delivers Trusted Insights for What’s Ahead®®. Founded in 1916, we are a non-partisan, not-for-profit entity holding 501 (c) (3) tax-exempt status in the United States. TCB.org

The next release is Tuesday, January 27 at 10 AM ET.

© The Conference Board 2025. All data contained in this table are protected by United States and international copyright laws. The data displayed are provided for informational purposes only and may only be accessed, reviewed, and/or used in accordance with, and the permission of, The Conference Board consistent with a subscriber or license agreement and the Terms of Use displayed on our website at www.conference-board.org. The data and analysis contained herein may not be used, redistributed, published, or posted by any means without express written permission from The Conference Board.

COPYRIGHT TERMS OF USE All material on Our Sites are protected by United States and international copyright laws. You must abide by all copyright notices and restrictions contained in Our Sites. You may not reproduce, distribute (in any form including over any local area or other network or service), display, perform, create derivative works of, sell, license, extract for use in a database, or otherwise use any materials (including computer programs and other code) on Our Sites ("Site Material"), except that you may download Site Material in the form of one machine readable copy that you will use only for personal, noncommercial purposes, and only if you do not alter Site Material or remove any trademark, copyright or other notice displayed on the Site Material. If you are a subscriber to any of the services offered on Our Sites, you may be permitted to use Site Material, according to the terms of your subscription agreement.

Trademarks "THE CONFERENCE BOARD," the TORCH LOGO, "CONSUMER CONFIDENCE SURVEY", "CONSUMER CONFIDENCE INDEX", and other logos, indicia and trademarks featured on Our Sites are trademarks owned by The Conference Board, Inc. in the United States and other countries ("Our Trademarks").

You may not use Our Trademarks in connection with any product or service that does not belong to us nor in any manner that is likely to cause confusion among users about whether The Conference Board is the source, sponsor, or endorser of the product or service, nor in any manner that disparages or discredits us.