Loading...

29 September 2023 / Brief

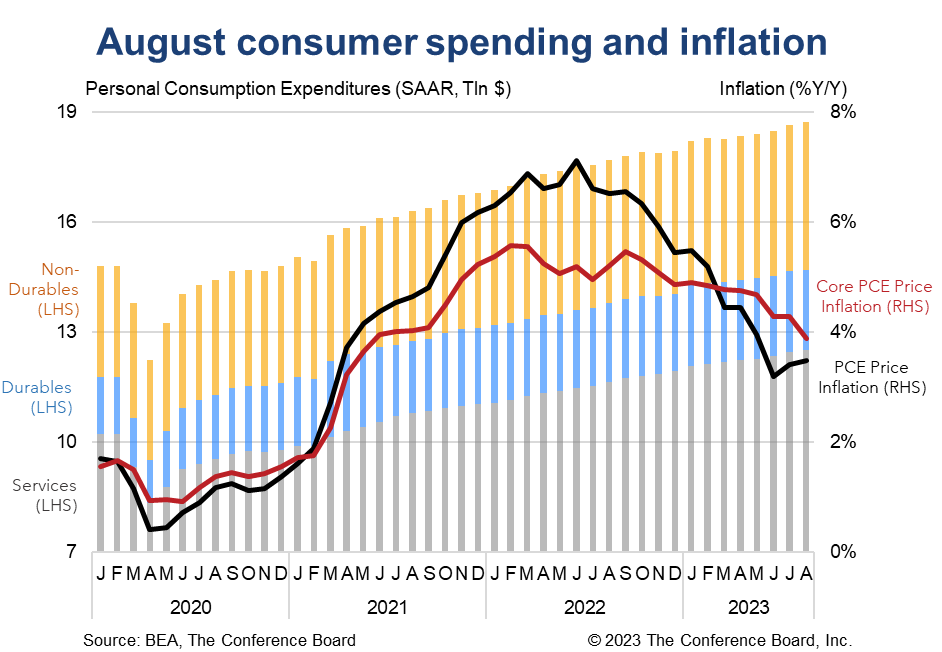

Consumer spending softened in August and real incomes were flat once again. Meanwhile, headline inflation increased due to a spike in energy prices, but core inflation continued to moderate. The Fed will likely be encouraged by this print—the economy is cooling. However, a prolonged increase in energy prices could be a major hurdle for the central bank. We continue to expect one final 25 basis point rate hike before yearend and no cuts until mid-2024. Our forecast for a short and shallow recession in early 2024 holds. Finally, a looming government shutdown will significantly curtail the release of economic data moving forward. The Fed (and the rest of us) will largely be flying blind until the situation is resolved. At first glance inflation appears to have accelerated in August, but that was largely due to a spike in gasoline prices. On a year-on-year basis the headline PCE deflator rose 0.1 percentage point to 3.5 percent. However, the core deflator dropped 0.4 percentage point to 3.9 percent. On a month-on-month basis the energy price impact is clearly visible in nondurable goods prices, which rose 1.4 percent from July. However, the trend in Core PCE (which excludes food and energy) was encouraging—up just 0.1 percent from the month prior. Overall personal income rose 0.4 percent m/m (in nominal terms) in August, vs. 0.2 percent m/m in July. However, when factoring in inflation, the real month-over-month growth rate was 0.0 percent m/m for a third consecutive month. In year-over-year terms, real personal income rose 1.3 percent in August, vs. 1.5 percent in July. Meanwhile, real disposable personal income (which is personal income less taxes) contracted by 0.2% m/m, vs. -0.2 percent in July and 0.0 percent in June. Finally, the savings rate fell from 4.1 percent to 3.9 percent of disposable personal income.

Highlights

Collectively, these data show that consumption remains on an unsustainable path. Personal incomes were flat on an inflation adjusted basis for a third consecutive month while real personal consumption expenditures continued to expand, albeit at a reduced rate. Meanwhile, the personal savings rate fell to 3.9 percent—the lowest rate since late 2022—and debt levels are quickly rising. In the background sits a rapidly diminishing pile of pandemic excess savings and mandatory student loan repayment begins in October. In our view, these trends will increasingly come to a loggerhead and an indebted and cash-strapped consumer will have to pull back. This is consistent with our expectation that a short recession is on the horizon.Inflation

Headline PCE price inflation rose from 3.4 to 3.5 percent year-over-year (y/y) in August and core PCE price inflation (which excludes food and energy) fell from 4.3 to 3.9 percent y/y. On a month-over-month basis (m/m), headline PCE inflation rose 0.4 percent and core PCE inflation rose 0.1 percent. Prices for goods rose 0.8 percent m/m (largely due to a 6.1 percent m/m increase in energy prices) and services rose 0.2 percent m/m.Incomes

Spending

Personal consumption expenditures rose by 0.4 percent m/m (in nominal terms) in July, vs. 0.9 percent m/m percent in July. Spending on services rose by 0.4 percent m/m while spending on goods rose to 0.6 percent m/m. After accounting for inflation, real consumer spending was up just 0.1 percent m/m in August with spending on services rising 0.2 percent m/m and spending of goods falling 0.2 percent m/m.

myTCB® Members get exclusive access to webcasts, publications, data and analysis, plus discounts to events.

Q2 GDP and June Inflation Support September Fed Hold

July 30, 2026

June CPI Closes the Door for July Rate Hike

July 14, 2026

May Spending Rebounds, but Inflation Takes Its Toll

June 25, 2026

FOMC Decision: There’s a Task Force for That

June 17, 2026